The Institutional Money Machine: Bittensor's Six-Step Loop

What happens when $10M enters the ecosystem, and who wins

The conference room on the 14th floor has a view of downtown but nobody’s looking at it.

Three people sit on one side of the table: the CFO, the head of alternative investments, and someone from legal who hasn’t said a word in 40 minutes. On the other side, their advisor from Mercer clicks to the next slide.

They’re reviewing the endowment’s 3% “emerging technology” allocation: $50 million that needs to go somewhere this quarter. Three options on screen:

a16z Crypto Fund VI - Standard venture exposure, 10-year lockup, minimum $5M.

Direct equity stake in an AI startup - High upside, high operational complexity, board seat required.

Yuma Total Market Fund - Something about “diversified exposure to decentralized compute infrastructure”.

The CFO interrupts. “Walk me through custody on number three.”

“Institutional-grade,” the advisor says. “Same structure as any other fund. Quarterly statements, third-party audits, full regulatory compliance. You wire dollars, you get exposure.”

“And what exactly are we getting exposure to?”

“TAO, that’s the base layer token. Plus a rebalanced basket of subnet alpha tokens. Think of it like an index fund, except instead of buying Apple and Microsoft, you’re buying decentralized compute capacity.”

The legal rep finally speaks. “Does this fit our mandate?”

“It’s infrastructure,” the advisor says. “Emerging tech, infrastructure play, diversified exposure. Checks all three boxes.”

The head of alternatives asks the only question that matters: “What’s the risk-return profile?”

Ten minutes later, they vote. Yuma gets $10 million.

Not because anyone in that room can explain what a subnet is or they believe at all in decentralization. Because the risk-return profile fits their mandate, the custody is institutional-grade, and the reporting matches their compliance requirements.

That allocation flows into dozens of subnets, including Chutes (SN64), which will process 9.1 trillion AI inference tokens this quarter. But the committee never discussed Chutes. They never discussed subnets at all. They discussed “diversified exposure to decentralized compute infrastructure.”

This is the moment Bittensor stops being a cool experiment and starts being infrastructure.

In June 2026, a subsidiary of Digital Currency Group launched the Yuma Total Market Fund. The pitch is dead simple: you give them dollars, they buy TAO and a basket of subnet alpha tokens, they rebalance quarterly. No wallets, no validators, no token mechanics. Just a quarterly statement like any mutual fund.

The technology doesn’t need to be understood anymore. It just needs to be accessible.

But before we look at how the money moves, we need to understand who is actually playing.

The Landscape: Who’s Actually Here

The institutional wave in Bittensor now contains real players with real capital deployed or vehicles live:

Yuma (DCG-backed): Launched October 2025 with $10M from Barry Silbert’s Digital Currency Group. Runs three funds: Total Market (TAO + subnet alphas), Subnet Composite (market-cap weighted index) and Large Cap (Mag7 for subnets).

Grayscale: GTAO trust trading OTC, spot ETF filed December 2025 (amended April 2026), targeting NYSE Arca.

DSV Fund (Siam Kidd): First 100% Bittensor-focused hedge fund. Kidd presented “Subnets as an Asset Class” at Proof of Talk 2026.

Others: Bitwise (parallel ETF filing), Safello/Deutsche Digital (European regulated staked TAO ETP), Stillcore Capital (US hedge fund), TAO Synergies (Nasdaq-listed, $750K into Yuma).

But nobody explains this well (or at all): When a billion-dollar allocator buys into Bittensor, where does the money actually go? What happens to the subnet developer building a decentralized weather model in their garage? What happens to the price of an alpha token?

And most importantly, what does this mean for you?

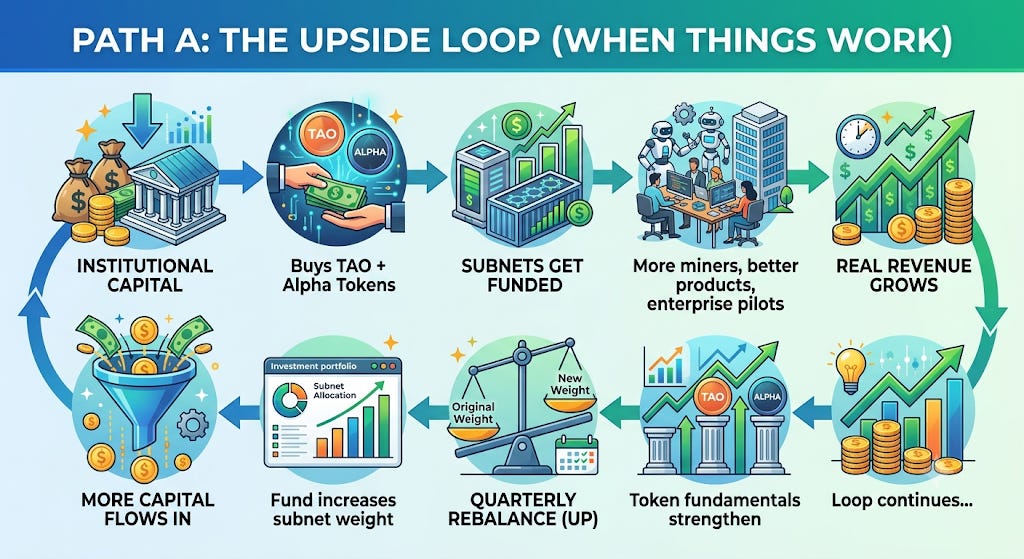

Following the Money: Six Steps from Allocation to Loop

Step 1: The Allocation

An institution, let’s call it the Oaktree Endowment, decides to allocate $10 million to decentralized AI. Their advisor recommends Yuma’s Total Market Fund because it’s the only product that gives them TAO plus exposure to the subnet layer without operational complexity.

Oaktree writes a check. They don’t fumble about trying to set up a Talisman, Crucible, or TAO.com wallet. They don’t have a notion of what a validator is. They simply get a quarterly statement, just like a mutual fund.

Step 2: The Fund Buys

Yuma takes Oaktree’s $10 million and deploys it across two layers:

Layer 1: TAO. The base token. This gets staked (likely with large, reliable validators), and the fund earns staking yield.

Layer 2: Subnet Alpha Tokens. This functions like an index. Think of it like the S&P 500, but instead of Apple and Microsoft, it’s Chutes (SN64), Targon (SN4), Vidaio (SN85), and the rest.

Step 3: The Subnet Gets Funded

Let’s follow the money into Targon (SN4), the decentralized AI compute platform.

Yuma buys Targon’s alpha token. Price rises 15% in a week. Now:

Miners expand GPU capacity - The token price rise makes mining more profitable, so miners add more hardware

Developers show up - A funded ecosystem attracts talent. Builders who were on the fence commit full-time

Marketing budget appears - Subnet owners can afford to attend conferences, sponsor hackathons, and land enterprise pilots

This is the initial capital injection. Money hasn’t turned into revenue yet, but the conditions for revenue are being built.

Step 4: The Fundamentals Improve

Six months later, those investments start paying off.

Targon now has 3x the compute capacity it had before Yuma bought in. The developer who joined in Step 3 shipped a confidential AI inference API that works with existing enterprise workflows.

An insurance company signs a 12-month contract for $250K. A biotech firm runs proprietary drug discovery models for $180K/quarter. By Q3 2026, Targon is generating $2M annually from paying customers.

That revenue gets routed back into the subnet’s incentive pool:

Miners earn more TAO and alpha tokens for providing compute

Validators earn staking yield

Alpha token holders benefit from buy pressure as revenue gets converted back to tokens

The token has moved beyond speculation to real revenue-backed yield.

Step 5: The Rebalance

Every quarter, Yuma rebalances the fund. If Yuma’s allocation framework is market-cap weighted, then subnets that grow faster will tend to receive larger weights over time, while smaller subnets will receive less.

Winners (subnets whose market cap grew) get more weight.

Losers (subnets that stagnated) get less weight.

This is the same mechanism that keeps Apple and Microsoft at the top of the S&P 500. Index funds don’t decide to buy more, they’re required to. The bigger you are, the more automatic buying pressure you receive.

Say Targon starts Q2 at 10% of the portfolio ($5M in a $50M fund). By quarter-end, Targon grows 40% while the overall market grows 15%. At rebalance, Targon gets 12% of what’s now a $60M fund, $7.2M instead of $5M.

That extra $2.2M comes from selling underperforming subnets.

Step 6: The Loop Perpetuates

Oaktree’s quarterly statement arrives. TAO is up 22%, the subnet basket up 18%. Each quarter’s performance determines the next quarter’s allocation.

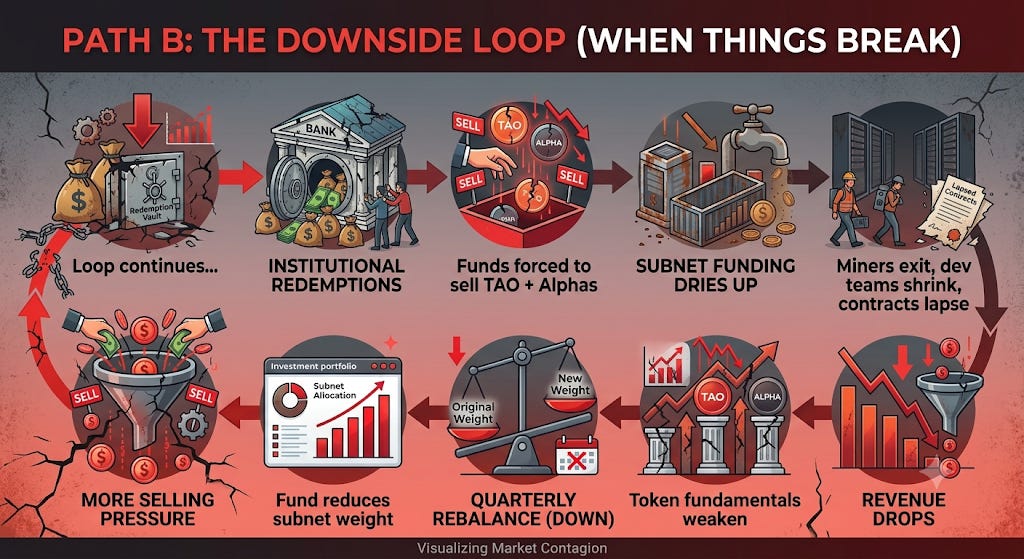

But this isn’t a straight line. It’s a loop that runs in both directions.

The Full Loop: Two Paths Forward

The same mechanism that creates exponential growth also creates exponential contraction. Here’s how both paths work:

What triggers this: Oaktree’s $10M becomes $11.8M. The allocation committee approves another $10M. Yuma rebalances up. Winning subnets get heavier weights. The next quarter starts with more capital than the last.

What triggers this: Oaktree’s $10M becomes $6.2M. TAO down 35%, subnet basket down 42%. If they’re mandate-driven (most institutions are), they rebalance down or exit entirely. The next quarter starts with less capital than the last.

What Determines Which Path?

Two factors:

1. Type of Capital

Patient Capital (endowments, strategic allocators): Rides through -40% drawdowns. 10+ year mandates.

Hot Capital (momentum funds, prop desks): Exits at -20%. Quarterly performance pressures.

2. Subnet Fundamentals

Real Revenue: Acts as a price floor. Customers don’t care about token price.

Speculation Only: No floor. Pure mark-to-market.

The dangerous combination: Hot capital + weak fundamentals = fastest downside spiral.

The safest combination: Patient capital + strong revenue = slowest downside, fastest recovery.

The Subnet Picker’s Dilemma

Where retail still has an edge is where the flywheel begins.

Many funds are market-cap weighted. That means they buy the biggest subnets. The subnets that are already winning.

Why? Because market-cap weighting is the only liquid metric available to a fund managing $50M+. They can’t diligence 128 subnets. They need a rule, and market cap is the rule.

Here’s what market-cap weighting ignores:

A subnet with real revenue but low token float.

A subnet with breakthrough tech but no marketing budget.

A subnet that’s growing 300% month-over-month but started from a tiny base.

The Institutional Blind Spot

Subnet A: $120M market cap, $5M quarterly revenue, 10% growth. It’s in Yuma’s fund.

Subnet B: $8M market cap, $1.5M quarterly revenue, 80% growth. It’s not in Yuma’s fund yet.

Subnet A is “safe.” Subnet B is mispriced with better fundamentals, but too illiquid for a $50M fund. If you have $5K or $50K, you can buy Subnet B. You can see what institutions can’t.

Three Strategies for the Gap

Here are three frameworks for finding subnets that benefit from the institutional wave without competing on market cap.

1. The Pre-Rebalance Strategy Institutional funds rebalance quarterly. But their research teams start looking at new subnets months before.

Identify subnets that are approaching the liquidity threshold to be included in the next rebalance. You want to buy before the fund does.

Look for daily trading volume crossing $100K+ consistently, market cap approaching the bottom of the current institutional basket, and real product or revenue beginning to materialize.

Example: A subnet ranked 15-20 today could enter the fund in Q4 if it crosses a liquidity threshold. Getting in at 18 is better than buying at 8 after the fund already did.

2. The “Revenue-First” Strategy Market cap is backward-looking; it reflects past attention. Revenue is forward-looking; it reflects whether anyone actually pays for the product.

Find subnets with the highest revenue-to-market-cap ratio—the ones generating real dollars but still undervalued by attention metrics.

Look for disclosed or estimable AI service revenue, enterprise clients or API usage growing, and a token price that hasn’t caught up to revenue growth.

Example: A subnet processing $500K/month in API calls but valued at $10M has a very different profile than a $100M subnet with no customers. The former is an operating business disguised as a token.

3. The “Niche Moat” Strategy Institutional funds need broad exposure. They can’t buy into hyper-specific subnets with small TAMs (total addressable markets). But that doesn’t mean those subnets aren’t valuable.

Find subnets dominating a niche that big compute providers ignore.

Look for unique data or compute offering (weather, biologics, edge devices, specific languages), deep domain expertise that can’t be replicated by generalist AI, and revenue from customers who have no alternative.

Example: A subnet doing decentralized drug discovery for rare diseases won’t be in Yuma’s fund. But it might have a $2M/year contract with a pharma company and zero competition.

Subnet Spotlight: Two Riding the Gap

Here are two subnets that illustrate the blind spot:

Vidaio (SN85): The Compression Leader

Ranked 1 for video compression efficiency in benchmark tests (June 2026).

Addresses a real market: video streaming costs are a $100B+ problem.

Currently small enough that it’s not in major institutional baskets.

If Vidaio starts hitting big revenue figures, it becomes an obvious rebalancing candidate. Getting in before that rebalancing is the play.

Zeus (SN68): The Weather Oracle

Ultra-precise weather data via decentralized sensor networks.

Serves agriculture, insurance, and logistics: industries that spend billions on weather data.

Scientific compute niche that generalist AI can’t replicate.

Niche moats like this don’t show up in market-cap indices. But they show up in enterprise procurement departments.

The Simple Rule

Here’s the one-sentence framework to take away:

Institutions buy market cap. You should buy fundamentals that haven’t become market cap yet.

The moment a subnet enters Yuma’s fund, the easy money is gone. The edge is in finding what gets there next.

The Deeper Question: Decentralized AI, or a New Goldman Sachs?

Bittensor’s entire value proposition is decentralized AI. But institutional capital is, by definition, concentrated. It is controlled by large allocators who deploy in size.

If a DCG subsidiary controls the largest fund, Grayscale controls the ETF, and a handful of validators control most staked TAO... are we actually decentralized? The April 2026 Covenant AI departure was partly sparked by these exact governance centralization concerns.

The reality is the Incentive design is what matters. Institutional capital creates price floors for alpha tokens and reduces sell pressure. This gives subnet teams runway to build products and generates healthy pressure to ship. Without institutions, alpha tokens are thinly traded and easily manipulated.

If the protocol can keep institutional influence on governance separate from their influence on price, it might work. The Root Reborn debate is happening exactly because the community is actively trying to figure out where validators should sit in the power structure.

Putting It Together: Your Action Checklist

If you only take three things from this issue:

Understand the loop. Institutional capital → subnet funding → product improvement → revenue → token support. It’s real, it’s happening, and it’s accelerating.

Don’t chase what’s already in the fund. Chutes and Targon are great subnets. But if you want edge, look at what’s approaching institutional thresholds, not what’s already there.

Use what institutions can’t Time, flexibility, and small-size access. A $50M fund can’t touch an $8M subnet. You can.

The fact that you can still buy the small sweaty startups on Bittensor while Yuma can’t is your proof the loop isn’t closed yet.

But watch the rebalance dates. The next quarter is always on the horizon and the next wave of capital is already being allocated.

Disclaimer: This is not financial advice. I am a writer documenting the Bittensor ecosystem. Always do your own research.