Machine Allocators Don't Want Your Best Guess

Inside Synth (SN50), the Bittensor subnet building risk infrastructure for agents trading millions

I was trying to plan my son’s outdoor birthday party last month. My phone’s weather app gave me a clean, confident prediction: mild and sunny. A single, reassuring data point. So I committed.

I rented the $300 bounce house, set up the tables in the garden, bought decorations that weren’t supposed to get wet, and waited.

1 PM arrives and exactly when nine hyperactive pre-schoolers were supposed to turn up, the sky turned the color of a bad bruise.

It poured.

Not a light drizzle. A full-blown downpour that turned our lawn into a swamp and left a bunch of sugar-fueled five-year-olds trapped in my kitchen, screaming at a decibel level that probably violated local noise ordinances.

The app wasn’t exactly lying; it just gave me a single guess instead of the full probability distribution.

Human beings crave clean, single-point answers. But the world doesn’t work in yes or no. It works in ranges and variance and fat tails. In finance, ignoring that variance isn’t just lazy. It’s how you get wiped out.

That exact gap, the distance between a comforting guess and raw probability, is where Synth (Subnet 50) steps in.

Inside the Swarm: How Synth Maps the Future

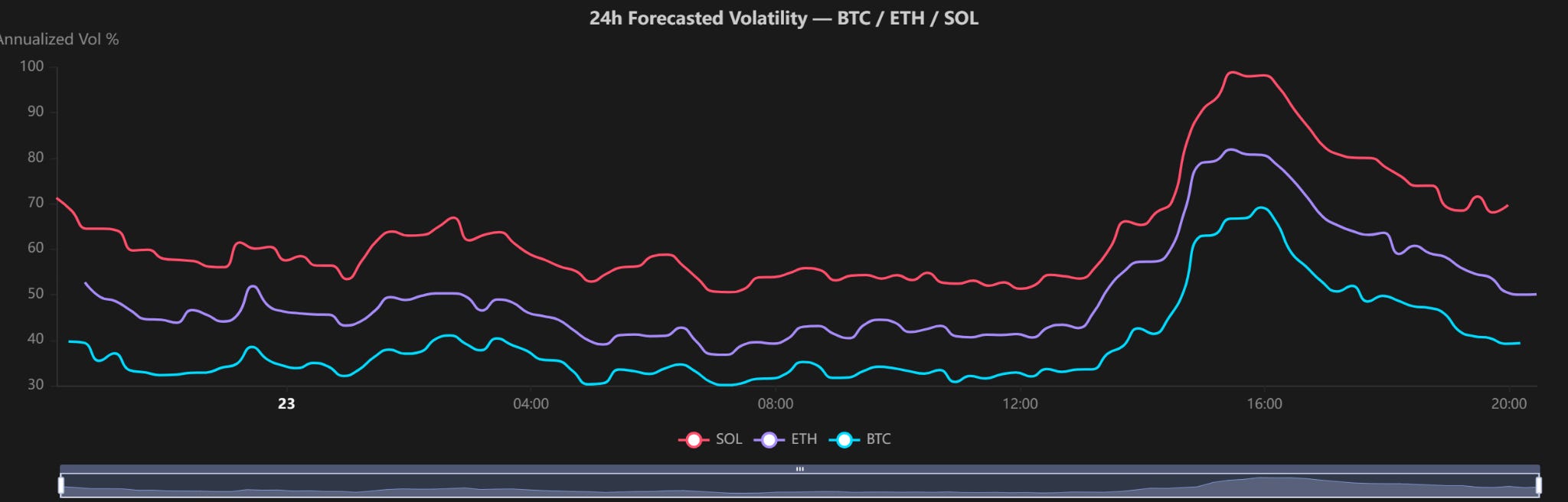

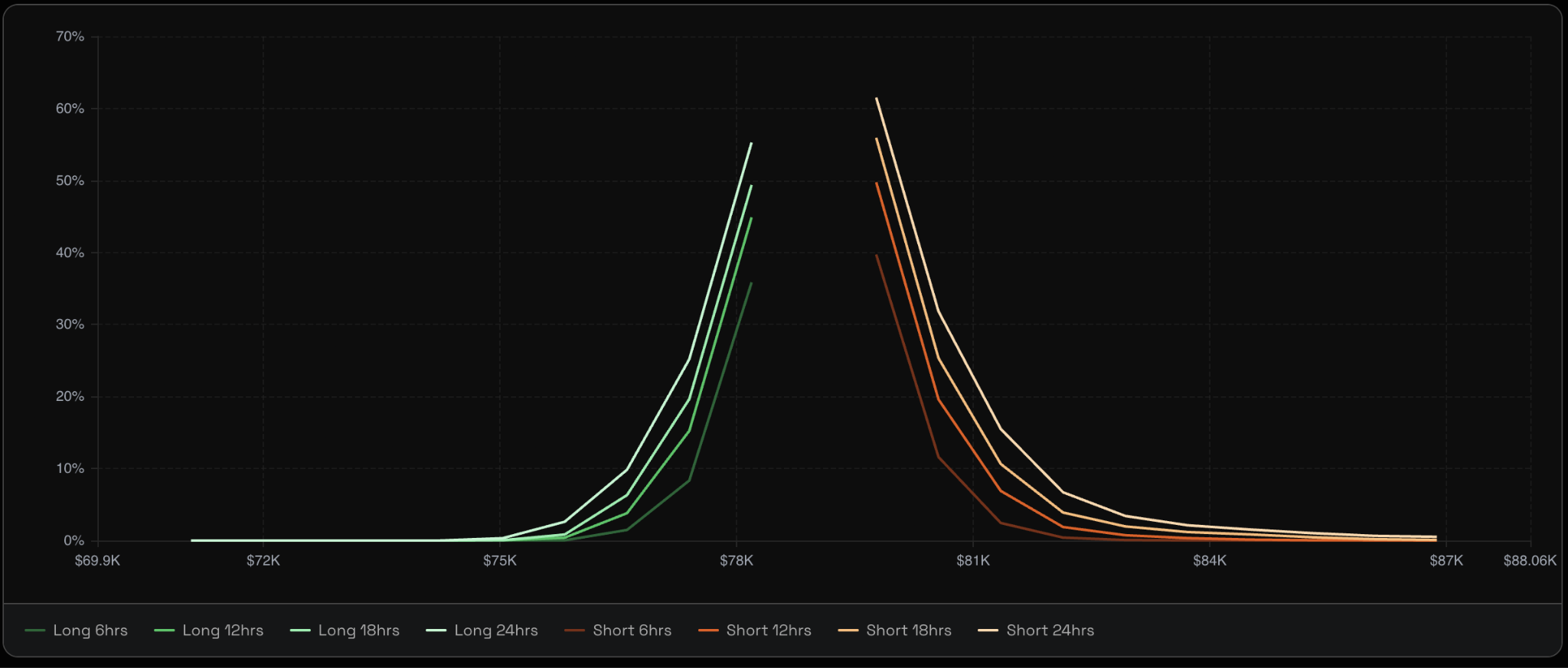

Most price-forecasting products give you a single number. “BTC hits $65k.” It’s like flinging one dart at a dartboard and hoping for the best. Synth gives you the entire dartboard, and tells you which sections are bigger.

Here’s how it works. Hundreds of miners submit 100 simulated price paths every 5 minutes. Validators score them using CRPS (Continuous Ranked Probability Score), which answers one question: how close was your probability cone to what actually happened? The output is a live API that computes liquidation probability at 6, 12, 18, and 24 hours.

As Synth’s founder James Ross puts it, modeling raw price is nearly impossible, but you can continuously improve at modeling volatility. He calls the subnet “the Olympics for Monte Carlo simulations.”

By shifting the goalposts from predicting a price to mapping a distribution (sharpened every five minutes by hundreds of models competing to be least wrong), Synth turns Bittensor’s raw compute into a pristine financial utility.

Why Now? The Rise of the Machine Allocator

In early 2026, prediction markets cleared over $20B in monthly volume.

But the bigger shift is the autonomous AI agents now trading real money on-chain.

A legacy oracle excels at telling an agent what an asset costs this exact second. But to size a massive bet or manage liquidation risk over a 24-hour horizon, machine allocators need deep statistical resolution: hundreds of models competing to be the least wrong.

Multiply hundreds of miners delivering 100 paths every five minutes across an entire asset index, and the network hammers out roughly 165 million high-resolution data points a day. The old way gave us a fragile guess, but the Bittensor way gives machine buyers the deep statistical map they actually need to survive.

It’s building the foundational risk API that the next generation of machine allocators, lending protocols, and DeFi agents will plug into to survive. Call it a new category: Risk Infrastructure.

Four Questions That Actually Matter

Let’s evaluate Synth the way a product manager would: through adoption signals, not just architecture.

Q1: What problem does it solve?

Anything making financial decisions on-chain is working from data that’s bad at the thing that matters most: tail risk.

Single-point guesses are close to useless for managing liquidations, sizing positions, or pricing options. A trader who acts on “BTC to $65k” has two outcomes: roughly right and a modest return, or wrong and annihilated. There’s no middle.

A trader who acts on a full distribution: “54% bullish, 90% confidence between $61k–$66k, fat-tail scenario at $52k” can size using the Kelly Criterion. Risk management transforms from paranoid guessing into a calculated, machine-readable routine.

Right now, miner behavior looks like it could mean two things: they’re building forecasts good enough to trade on, or they’re optimizing for protocol rewards. We can’t distinguish between the two from public data yet. Until we see live trading results or independent performance audits, the demand is largely based around the protocol paying miners who produce output the protocol consumes.

Q2: For whom?

Two tiers. Quant traders and options pricers are the primary market; on-chain DeFi and AI agents are the secondary. This is a power-user product for hedge funds, options desks, perpetual DEXs, and autonomous trading agents moving millions without human oversight.

The go-to-market advantage is Mode, the Ethereum L2 that co-founded Synth and serves as a built-in first customer, wired into its AI Terminal and DeFAI agents:

Most subnets die because they build a product and then go looking for customers; Synth built the product inside a customer. But if Mode is both builder and principal consumer, much of the apparent demand is captive, not independent validation. Synth shows signs of external monetization, but no public evidence yet demonstrates meaningful demand separation from Mode.

There’s a hidden third tier Ross emphasizes: ML teams training financial models. Synth’s daily data isn’t just for querying, it’s for training. Historical data leads to overfitting; synthetic data generates the edge cases that matter in live markets. A quant team that bakes Synth’s data into its model weights isn’t switching APIs easily. That’s a stickier, harder-to-commoditize relationship than query-time consumption.

Q3: How big is the opportunity?

A narrow SAM of approximately $2.5B in alpha signals and alt data, with a broader TAM of around $44B as DeFi and autonomous systems adopt better forecasting infrastructure. But data and oracle markets are notoriously hard to monetize, and the gap between a $44B opportunity and a $6M market cap only narrows if Synth can capture value, not just create it.

The core pain is that traders, protocols, and agents need dependable forward-looking signals that fit into live decision workflows. Synth is solving that by making forecasting a repeatable product loop: users get probabilistic outputs, miners compete to improve them, and the four-week Polymarket trial in October 2025, which returned roughly 110%, provides an early signal that the workflow can create measurable value.

There’s also an expansion vector the $44B doesn’t capture: Synth as a dependency inside the Bittensor subnet graph itself.

If composability becomes real, any subnet touching financial data needs a risk input: take a trading-agent subnet querying Synth for liquidation probabilities, or a lending subnet using it for collateral scoring. If Synth becomes the risk oracle in that stack, the addressable market is every financial subnet on Bittensor. Whether that happens depends entirely on the team's execution discipline: the current plan to calculate operating costs and redirect revenue to buybacks puts all value capture in their hands.

Q4: How will we know if it’s working?

We’ll know Synth is working when external users choose it as forecast infrastructure, not just when the internal network is active.

The clearest signal is independent API consumption: usage from traders, protocols, and agents outside the Mode ecosystem, with repeat integrations over time.

The second signal is out-of-sample performance across many trials and asset classes, showing that forecasts remain useful in live conditions rather than only in backtests or one-off wins.

On the supply side, we should see sustained miner participation from teams that consistently perform well, with weak speculative strategies filtered out through weekly reporting, immunity periods, and reward persistence.

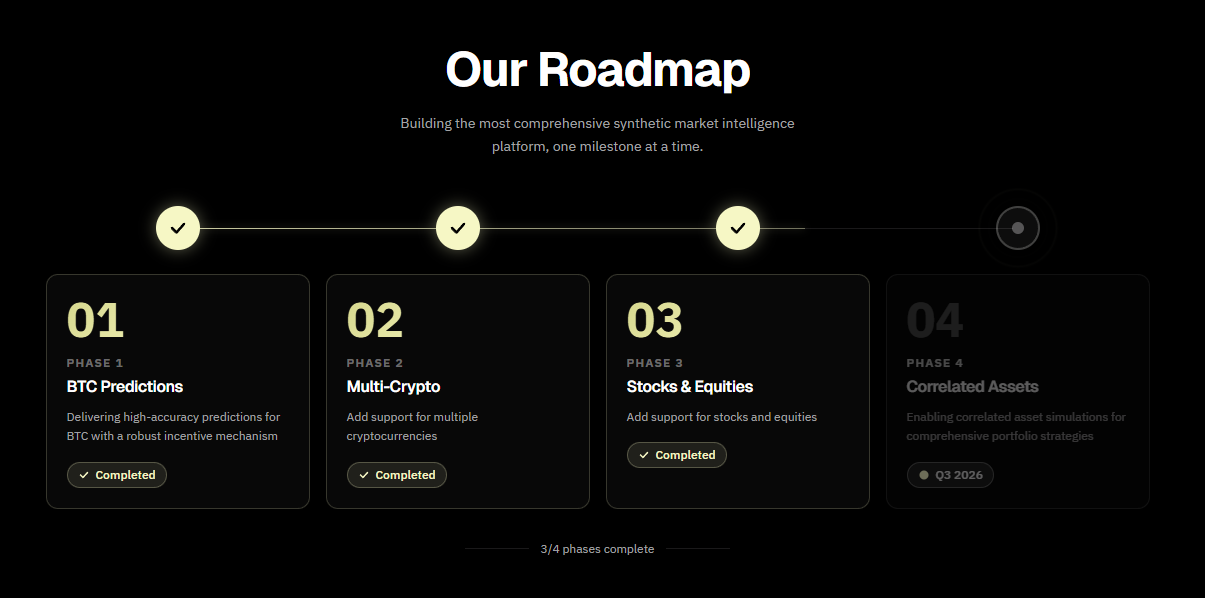

Roadmap execution matters too: adding new assets (recently equities), shorter time horizons, and eventually more use cases should expand both demand and supply without degrading forecast quality.

The Takeaway: Bull vs. Bear

The bull case: Synth is the first financial subnet selling a better question, not just a better answer. It has a working product, a built-in customer in Mode, and hidden upside in ML training-data lock-in. If subnet composability happens, Synth becomes the default risk oracle. A $6M market cap against a $44B TAM is real asymmetry.

The bear case: Value creation isn’t value capture. Deep options markets already do this well. Mode’s demand may be captive. And if miners truly had a superior edge, they’d trade on it rather than farm emissions.

Synth is the most legitimate financial subnet on Bittensor right now. But the only number that confirms product-market fit is independent API consumption. When non-Mode entities start paying for this data, it shifts from a well-engineered project to an undeniable market force. Everything until then is promising but unproven.

The Bounce House Question

Back to the birthday party: that weather app didn’t give me a distribution because I didn’t want one. I wanted the comforting answer. The clean “yes” that let me rent the bounce house and move on. The app sold me certainty, and I bought it. Then I spent an hour hosing cake frosting off my kitchen walls.

If it had shown me the real distribution, let’s say 70% mild, 20% light rain, 10% biblical downpour, I still might have rented the bounce house. But I would have set up the backup plan, maybe bought indoor some decorations. Carried the variance instead of pretending it didn’t exist.

That distance, between the answer we want and the distribution we actually need, is where Synth lives.

The real bet isn’t that miners can beat options desks. It’s that the next million financial decisions on-chain won’t be made by humans who crave clean answers, but by machines that require dirty, honest, high-resolution probability.

Now, for me, the accessibility tension is still real. The subnet that figures out how to show probability distributions to someone who doesn’t know what CRPS stands for is the one that breaks out of the quant ghetto. Making probability visual is making probability adoptable.

But every piece of infrastructure that changed the world started as something nobody understood. TCP/IP was impenetrable, while HTTP was academic. Technology that matters arrives as a necessary first, and then the builders who survive figure out the translation layer.

So I’ll leave you with this: if you could see the full probability distribution for one decision in your life: your mortgage, your portfolio, your kid’s college fund, would it change what you do? Or would you still reach for the comforting answer?

The gap between those two responses isn’t just Synth’s market. It’s the entire gap between the world we live in and the world we’re building.

Disclaimer: This is not financial advice. I am a writer documenting the Bittensor ecosystem. Always do your own research