Exit Strategy or Exit Scam?

Inside Covenant AI's Departure from Bittensor

On April 9th, Sam Dare published a letter accusing Bittensor of being a lie.

It was long, carefully written, and timed for maximum damage. It arrived alongside a purpose-built whistleblower website and a coordinated dump of $11 million in subnet alpha tokens, most of it sold the night before the letter went public and before his own community had any idea what was coming.

Let me walk through what happened, what I think it means, and why I’m not selling.

Reconstructing the Exit

For readers newer to this ecosystem, some context.

Covenant AI was not a fringe player. The team operated three subnets on Bittensor: Templar (SN3), Basilica (SN39), and Grail (SN81). Templar was the crown jewel: a decentralized pre-training environment that produced Covenant-72B, a 72-billion-parameter model trained across more than 70 independent contributors on commodity hardware and coordinated through the Bittensor incentive layer.

The achievement was real. NVIDIA CEO Jensen Huang praised it publicly. Chamath Palihapitiya mentioned it on the All-In podcast. TAO rallied 90% in the month that followed. It was a mainstream moment for Bittensor, the proof of concept the whole ecosystem had been working toward.

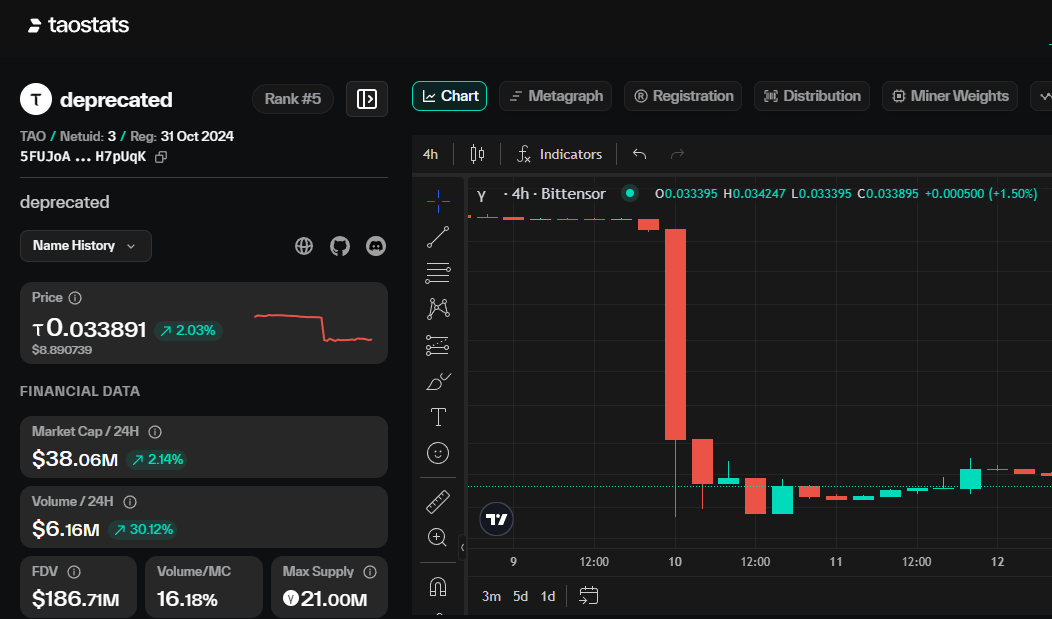

Then, on April 9th, Sam Dare, the founder of Covenant AI, posted his open letter announcing the withdrawal of his three subnets from the Bittensor ecosystem. TAO dropped 27% in two hours with nearly $900 million in market cap evaporated.

Dare’s letter laid out four specific allegations against Bittensor co-founder Jacob Steeves, known universally in the ecosystem as Const.

He alleges Const had:

Suspended emissions to Covenant’s subnets.

Removed the team’s moderation capabilities over their own community channels.

Unilaterally deprecated their subnet infrastructure.

Applied economic pressure through large, visible token sales timed to moments of conflict.

Explosive claims, but before we get to Const’s rebuttal, it’s worth understanding how Bittensor’s emission mechanics actually work. Because this is the technical detail that makes or breaks the most serious accusation.

Under dTAO, emissions are determined entirely by an on-chain algorithm. There is no admin key or pause function.

Each subnet’s share of daily TAO emissions is set by net TAO flows into its liquidity pool calculated automatically by the protocol, in the same way for every subnet without exception.

What Const can do, what any TAO holder can do, is buy or sell alpha tokens in those pools. When he sold his positions in Covenant’s three subnets, that reduced TAO in the pools and affected the flow-based emission calculation. The same way anyone’s sell would.

This is market mechanics at work. Emissions cannot be modified in any other way. Dare’s central accusation requires a technical capability that does not exist in the protocol.

Const addressed each claim directly. He stated:

He has no authority to pause emissions (as described above).

He did not remove Dare’s moderator role outright, but removed his ability to delete posts and later restored it. Community member Alex DRocks corroborated in real time, it was Dare who deprecated his own Discord channels, and the posts deleted were questions from community members asking why SN39 was replicating work another compute subnet had already done. Dare was deleting scrutiny.

He’s unsure what deprecating their subnet’s infrastructure actually means (yet to be confirmed).

His token sales (less than 1% of what he had invested in Covenant’s teams) were made because Covenant’s subnets were not running and were operating on near 100% burn code, affecting emissions the same way any buy or sell would.

The Rug Frame: Reading Sam Dare’s Exit Clearly

Now pay attention to the choreography.

On the same day as Dare’s open letter, a newly launched site called Tao Papers published internal documents and on-chain forensics from multiple whistleblowers.

The headline claim: of 41 network upgrades carried out between 2023 and 2026, 38 were proposed, signed, and deployed entirely from infrastructure controlled by Const, with the other two signers approving each upgrade within minutes and no public discussion on record.

Taken at face value, that’s worth examining properly.

But it is not spontaneous. You don’t build a forensic website overnight.

The fact that the open letter and the whistleblower site launched simultaneously tells you everything about the intent. This was a campaign planned and timed for maximum narrative impact on exit.

And the exit was the most malicious part.

Prior to the public announcement, Dare had already sold 37,000 TAO ($11m) worth of subnet alpha tokens across Templar, Grail, and Basilica.

The dump hit retail holders tied to Covenant’s projects before they had a single word of warning.

TAO’s sales volume had already reached its highest level since December 2024 in the 24 hours before the letter went public.

This was not a principled departure, but an exit strategy, wrapped in governance language, timed for maximum extraction.

The Tao Papers data may contain real information about governance concentration, but its framing as independent corroboration collapses the second you notice it arrived gift-wrapped, synchronised with the open letter, hours after the pre-announcement dump had already cleared.

The Legitimate Critique Underneath the Drama

Let me be honest here, because this newsletter does not earn your trust by only telling you what you want to hear.

The Tao Papers governance data, whatever you think of Sam Dare’s motives, raises a legitimate question about Bittensor’s current governance structure.

38 of 41 network upgrades originating from a single founder’s infrastructure, with co-signers rubber-stamping within minutes, is not the picture of distributed governance.

The triumvirate structure, as currently operating, functions more as a legal architecture than a genuine check on centralized decision making.

Const has not explicitly addressed that structural critique. He responded to Dare’s specific allegations point by point. He did not address the broader claim that meaningful governance authority has not yet transferred.

I think that’s intentional, because his response is in line with a design pivot. His statement in the aftermath of the exit:

“This will prove to birth the first subnets on Bittensor that run headless and as true commodities.”

These are the words of a builder saying the criticism identified a real structural dependency, and the answer is to architect it away.

The reality is, decentralization is a gradual process for the good of the protocol.

Every major network retains concentrated authority early to move fast and prevent paralysis, then systematically transfers power as architecture matures. That transition creates friction. Big players in the ecosystem: subnet founders, major investors, validators, all have different timelines for when centralization should end.

When those views collide with financial stakes this large, exits like Dare’s become possible.

Const stepped down as CEO of the Opentensor Foundation two months ago, explicitly to push decentralization forward. This episode accelerates that trajectory.

Revealing a structural weakness is different from being terminally broken. Every serious protocol has gone through this and now we will see how the Bittensor ecosystem responds.

The Road to Full Decentralisation: What Changes Now

The specific structural reform announced in the aftermath of this crisis is worth understanding clearly, because it directly addresses the failure mode that Dare exploited.

Bittensor is introducing lock-based subnet ownership.

The mechanics: ownership of a subnet will be determined by a team’s long-term economic commitment, not just their technical presence.

Investors will have transparent, advance notice if a subnet owner unlocks their tokens, allowing the market to reprice before founders can use their communities as exit liquidity.

The system will also allow investors to shift their staked capital fluidly to alternative management teams.

If lock-based subnet ownership had existed on April 9th, every holder in Templar, Basilica, and Grail would have seen the unlock coming before the dump hit.

The market would have repriced on Dare’s decision to exit, not on his public announcement of it. The $900 million wipeout would have been a controlled, visible repricing rather than a midnight ambush.

Autonomous, headless subnets, running as true commodities without a single operator as a point of failure, are the longer-term architectural answer. The Covenant crisis exposed a network that is mid-decentralization, under pressure and now moving faster.

Stillcore Capital (Bittensor Fund) partner Mark Jeffrey put it plainly:

“Bittensor is a quite a lot more than Subnet 3, and TAO will carry on fine without it.”

He is right. And multiple big players have come out in support of Const in the aftermath of this incident. But I’d go further.

Bittensor is stronger for this than it was two weeks ago. The lock-based model and the headless subnet architecture were coming. This crisis brought them forward.

What Happens Now for Covenant and the Three Subnets

Covenant operated three subnets: Templar (SN3), Basilica (SN39), and Grail (SN81). Templar was the crown jewel — the pre-training environment that produced Covenant-72B. Basilica was focused on decentralised compute. Grail handled more complex task-driven AI workloads. All three now show as deprecated on Taostats, removed from active participation in the network.

The team will continue developing Covenant-72B off-network, with new project announcements promised but no ecosystem named.

They’ll be building without the TAO incentive layer, without the established subnet infrastructure and carrying the reputational weight of what much of the community now views as a coordinated exit dump.

New investors in whatever comes next will be asking the same question Bittensor holders are asking today: who’s really in control, and when are they planning to leave?

For Bittensor, the three subnets now need transition to new operators or a headless model, and the process is untested at this scale. If the transition is messy, it reinforces the single-point-of-failure narrative.

If it goes smoothly, it validates Const’s “true commodities” vision: that subnets should eventually run without any dependency on their founding team.

That transition is the first real test of everything Const said would come next. I’ll be watching it closely.

What the Price Action Was and What It Wasn’t

When a high-profile governance headline breaks alongside a prominent team exit and a visible token dump, the market reacts predictably.

Traders operating on shorter timeframes, whether that’s algorithms, momentum players, or simply anyone with a stop-loss or a risk tolerance that got breached, will sell into uncertainty.

Not because they’ve evaluated whether Sam Dare’s accusations are credible or Const’s rebuttals hold up. Because uncertainty itself is the signal.

Even longer-term investors who might otherwise hold through volatility often reduce exposure when a story that felt clean suddenly feels complicated. They’re not abandoning their thesis necessarily, they’re stepping back until the fog clears.

That is also rational behavior. Preservation comes before conviction when the facts are in dispute.

Your job, if you hold TAO with conviction, is not to front-run these reactions or predict when sentiment will stabilize.

It is to ask different questions entirely:

Has the network stopped working?

Has the underlying technology been invalidated?

Has anything happened here that changes the fundamental thesis?

Has the team with the long-term vision left, or the team that just cashed out?

Those are the questions that matter. The price tells you what the market did on April 9th. It does not tell you what TAO is worth in 2027 and beyond.

Ecosystems Have Always Had Bad Actors: The Price of Upside

Here is what I want non-crypto readers to understand. And what I want crypto natives to remember.

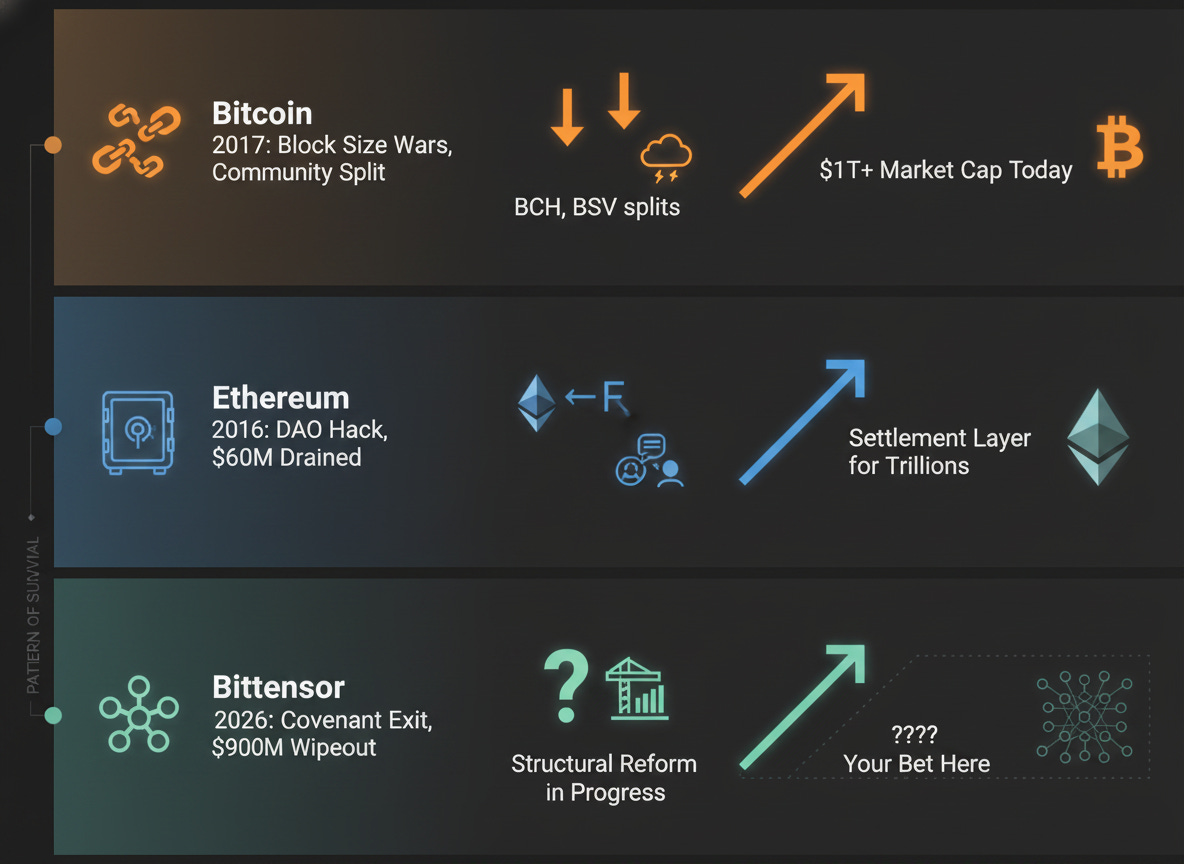

Every transformative decentralized network has had this moment. More than once.

Bitcoin didn’t emerge from consensus and goodwill. It emerged from years of the block size wars, a community riven between competing visions, ultimately splitting into Bitcoin and Bitcoin Cash, and then Bitcoin Cash splitting again into Bitcoin Cash and Bitcoin SV, driven by Craig Wright’s years of fraudulent Satoshi claims, litigation, and manipulation.

Those were genuine existential moments. Bitcoin absorbed all of it. The network is worth over a trillion dollars today.

Ethereum’s defining early crisis was the DAO hack in 2016. A vulnerability was exploited, $60 million drained, and the community faced an impossible choice: honor the immutability they had promised, or fork the chain to recover the funds. They forked. Half the community followed.

The other half stayed on the original chain and called it Ethereum Classic. People said Ethereum would never recover its credibility. ETH is now the settlement layer for trillions of dollars of financial activity.

The pattern is consistent. Early-stage decentralised ecosystems attract the most visionary builders and the most opportunistic actors simultaneously, because the rules are still being written.

Power is concentrated by necessity before it can be distributed by design. And some people see that window and take it.

This is the cost of being early to asymmetric upside.

If you wanted zero drama and full governance maturity, you would be buying index funds. You are here because the upside on the early innings of decentralized AI infrastructure is unlike anything in a passive portfolio.

That upside does not come without episodes like this one.

Reading the Aftermath

What This Builds

Lock-based ownership is a genuine structural improvement, not a PR response. The headless subnet architecture, if it delivers, creates a more resilient and more trustworthy system than what Covenant left behind. The ecosystem survived one of its largest subnet’s exit without collapse.

What to Monitor

Watch two things.

First: how cleanly SN3, SN39, and SN81 transition. Smooth operator handoffs would validate the true commodities thesis and demonstrate that Bittensor’s incentive layer is more durable than any single team.

Second: where Covenant deploys next. If they name a competing ecosystem, the protocol-switching cost argument becomes live and worth monitoring.

What Remains Unresolved

The triumvirate governance concentration is real and not yet fully resolved. Const’s point-by-point rebuttals were credible. The structural critique has not been fully answered. Further prominent departures, especially if they cite similar governance concerns, would compound the credibility damage faster than any structural reform could repair it.

What Dies Here

The narrative that any single subnet team is Bittensor. This moment definitively ends that story, which is uncomfortable in the short term and healthy in the long term. The ecosystem should never again be this exposed to a single founder’s exit.

The Morning After

There is a difference between having a genuine grievance and performing one for maximum effect.

Real concerns deserve real processes. You don’t burn the room down to prove the room had a fire hazard. And when someone times their concern to the moment of maximum personal extraction, you learn important things about them more so than their peers.

The Bittensor network is still running. The technology that produced Covenant-72B still exists, built on infrastructure that no departing team can take with them.

The builders who stayed chose to stay. And the structural reforms now in motion were always where this ecosystem was heading.

The price will do what prices do. I’m watching the transitions.

Until next time.

Cheers,

Brian

Disclaimer: This is not financial advice. I am a writer documenting the Bittensor ecosystem. Always do your own research.

Why has no one done any analysis of 'futures' shorts or 'options' puts on TAO in the period leading up to the cash out? Quite honestly I do not even know if they exist as they are outside my ballpark. But if they do, they should be very closely examined for the possibility of 'untoward' activity. Let me be clear - I am NOT making any accusations here. I'm just stating that if exchange methodology for shorting TAO existed before this very public cash out, then it should be examined extensively and a report should be presented to the community.

Brilliant breakdown, Brian. You completely cut through the noise. I agree 100%: shaking out opportunistic actors and forcing structural upgrades like lock-based ownership will ultimately make the TAO ecosystem much stronger. This is exactly the kind of stress test a maturing protocol needs. Thanks for keeping us up-to-date!